Reform of the global financial architecture: the struggle between the Global North and Global South

The United Nations has put forward ambitious proposals to reform global economic governance ahead of the Summit of the Future, but in the current climate of geopolitical rivalry and strategic competition many of them are unlikely to achieve the required consensus. Reforms that are seen as the relinquishment of a privilege on the part of some powers to the benefit of others will be more limited, though those aimed at improving debt management and financing for development do appear attainable.

In the summer of 1944, in a village north of New York called Bretton Woods, delegations from 44 countries gathered for the United Nations Monetary and Financial Conference to lay the foundations of the future international financial architecture. The goal was to foster open markets, temper economic nationalism and promote the reconstruction of economies after the Second World War, although the new design of economic governance gave the allied industrialised countries control over the system and the production structures. Fixed exchange rates against the US dollar and gold were introduced, and the United States became the biggest shareholder (with power of veto) in the World Bank and the International Monetary Fund (IMF), newly created institutions whose chiefs since than have always been from the US and Europe, respectively.

The system has evolved over the last 80 years, but the changes have been ad hoc, in response to economic and political crises and made largely to suit the needs of the big Western powers. A clear example of that came in 1971 when the United States chose to leave the gold standard and change the international monetary system unilaterally in order to fund the Vietnam war. But the changes introduced in recent decades were not designed to adapt economic and financial governance to a post-colonial, globalised world that has 149 more nations than when the Bretton Woods institutions were created.

Today, the expression “international financial architecture” refers to the current set of financial frameworks, regulations, institutions and markets that safeguard the stability and operation of global monetary and financial systems. Apart from the original institutions like the IMF or the World Bank, the actors that make up this architecture today include public financial institutions such as development banks; private financial regulation bodies like the Basilea Committee on Banking Supervision; informal groups of norm-setters, such as the G7 or the G20; formal but non-universal norm-setting bodies like the Organisation for Economic Co-operation and Development (OECD); groups of sovereign debt creditors such as the Paris Club, or the United Nations itself.

All these institutions, however, have something in common: they lack effective representation of developing countries. And global coordination as it stands clearly does not suffice to promote investment and sustainable development, remove inequality and systemic risk, or support the 2030 Agenda. In the words of United Nations Secretary-General António Guterres, “the global financial architecture is outdated, dysfunctional and unjust, incapable of adapting to the multipolar world of the 21st century”. To meet this challenge, a United Nations policy brief has put forward a series of reforms for adoption at the Summit of the Future, to be held in September 2024.

Proposals to enhance legitimacy and transparency

For the Global South, which is represented at the United Nations by the Group of 77 (G77), the priority in the reform of the financial architecture must be to adjust the voting power and the governance structures in the international financial institutions (IFIs) in order to broaden developing countries’ effective participation in decision-making processes and open up their access to resources (Pedroso Cuenca, 2023). This demand, which is directed at the World Bank and the IMF in particular, already featured in the Monterrey Consensus in 2002 and is Target 10.6 of the Sustainable Development Goals (SDGs) established in the 2030 Agenda. There has been little progress in this area, however (Martens, 2023).

Some scholars think it is near impossible for the United States to allow its share of votes in the IMF to drop below 15% and thus lose its veto power, because it would be seen as a concession that favours China and the agreement would have to be ratified by US Congress. The countries from the Global North are more interested in broadening the organisations’ mandate for the provision of global public goods such as the fight against climate change or pandemics. It is a proposal that the Global South eyes with suspicion, fearing it will divert development financing funds or result in new conditions on accessing them.

The summit policy brief also underscores the need for greater regulation of the global financial markets. Namely it states that the most pressing matter is to tackle the non-bank financial sector, which currently accounts for over 50% of total global financial assets yet acts outside the most stringent banking regulations. It proposes applying the principle of “same activity, same risk, same rules” to address risks to the stability and integrity of the financial system, as well as speeding up and stepping up efforts to adapt the financial markets to the SDGs.

While it is a commendable goal, analysis of the concrete proposals reveals the difficulties in putting them into effect. Because the question is this: does the United Nations have the mandate to tell the IFIs how they should be run? For this proposal to come to fruition requires the United Nations and these institutions to coordinate and there would have to be a consensus among the main actors involved. In this case, the discrepancies are not so much between the Global North and Global South, but rather among the countries of the Global North, who have notable differences over how to regulate capitalism.

Proposals to increase countries’ resources

The second priority for the G77 countries is to tackle the reform of the financial safety nets that come into play in the event of a crisis. The IMF has a central role here as a lender of last resort through its special drawing rights (SDRs), which allow countries access to unconditional liquidity. If a global crisis strikes, the IMF allocates new rights to countries in proportion to their quotas in the institution. This means that until 2009 over a fifth of IMF member countries had never received an SDR allocation and that, in 2021, in the biggest issuance in history in response to the COVID-19 pandemic, developing countries only received around a third of that liquidity; the main beneficiaries were the richest countries (United Nations, 2023: 21).

Given these circumstances, the Summit of the Future policy brief sides with the G77 in its call for SDRs to be issued automatically in the event of exogenous shocks, and for allocations to be based on a country’s needs, not its quotas in the IMF. In order to avert countries’ rejection of increases in their contributions to the IMF, it makes the case for selling part of the institution’s gold reserves. Valued at historical cost, they could generate $175bn in realised gains.

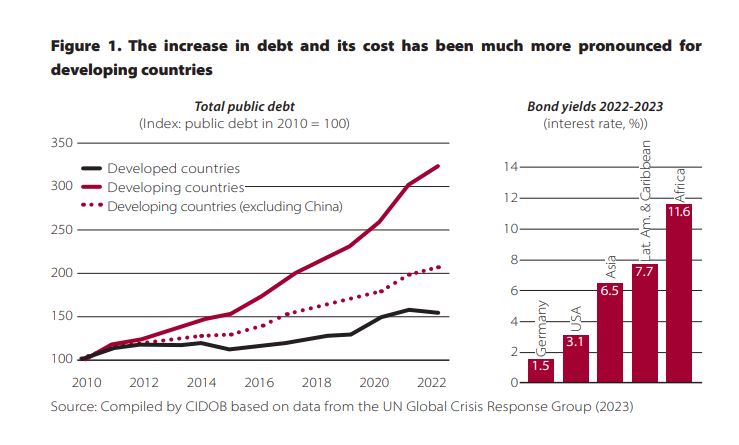

Third, the G77 urges tackling the management of external debt. Debt service (repayment of the principal and interest) is at record levels as a result of the pandemic, the war in Ukraine and the increase in interest rates (see Figure 1). What is more, developing countries now depend more on private creditors, such as investment funds, and non-Western official bilateral creditors, like China. This has helped to drive up the cost of borrowing and make debt restructuring more complex.

So far, multilateral responses to debt problems such as the Debt Service Suspension Initiative or the Common Framework for Debt Treatments, have proven insufficient. Given this, the summit policy brief proposes, for one thing, lowering debt-related risks through measures such as the creation of sovereign debt markets that support the SDGs and, for another, reforming current debt restructuring processes.

The creditor states in the Global North are aware of the need to tackle the debt problem but feel no urgency to do so because this crisis mainly affects countries with which they have very limited trade and financial ties; what are judged to be “countries that pose no systemic risk” (those that do not matter). In addition, they fear that restructuring the debt will make it easier for these countries to meet their debt obligations to China, and they reject extending the renegotiating framework to middle income countries because of the costs involved. China, for its part, has no wish to see its debt play a subordinate role to that of the Paris Club and is more inclined to renew loans than undertake a restructuring.

Fourth, the G77 has spoken in the United Nations to make an urgent call to recapitalise the multilateral development banks and attract private capital (blended finance) in order to improve borrowing conditions for nations of the Global South and achieve the Sustainable Development Goals. These proposals are very much in line with those the United Nations has made for the Summit of the Future, where the aim is to promote changes in the multilateral development banks so that they lend at least $500bn a year, double the current amount.1

Last, but no less important, is the issue of reforming the global tax architecture. Illicit financial flows cause losses close to $500bn a year, mostly due to tax evasion and avoidance by multinationals. This has a disproportionate effect on developing countries given their greater reliance on corporate income tax.

After years of vagueness, the need to finance increased spending arising from the pandemic prompted 140 countries to reach an OECD-led landmark agreement in 2021 to ensure multinationals pay more tax. But the initiative has been heavily criticised on account of the considerable delays in implementing it, its lack of transparency and because the countries of the Global South were left on the sidelines when devising the measures. That was why the African bloc in the United Nations proposed creating a broad binding framework on international taxation within the organisation, and not only focused on taxing multinationals. Significantly, the Global North voted in bloc against the resolution, which passed with the support of 125 countries from the Global South.

The aim at the Summit of the Future is to push for (i) simplified global tax rules, as developing countries prefer straightforward approaches; (ii) a higher global minimum corporate income tax rate, and (iii) the creation of non-reciprocal tax information exchange mechanisms to benefit developing countries. Currently, the European Union (EU) only supports United Nations rulings on tax issues being non-binding, allowing them to protect tax havens (most of which are in Europe) and control over their tax regimes.

Outlook

The search for the consensus required to underpin the decisions may dilute the Summit of the Future’s ambition and scope, all the more so in an international climate of geostrategic competition and heightened political polarisation. In the areas where there is a greater divergence of interests between the Global North and Global South, such as those related to governance, tax reform or non-bank regulation, the agreements may be more limited, while it is more likely there will be meaningful progress in those where the interests of the major powers converge.

In any case, it is hard to change the development paradigm without tackling a reform of the rules of global commerce, their governance (the cause of the current deadlock in the World Trade Organisation, WTO) or the developing countries’ unequal access to technology and property rights, all of which are demands of the Global South that have been left out of the summit’s policy brief.

Bibliographical references

Martens, Jens. “Reforms to the global financial architecture” | Global Policy Forum. Global Policy Forum Europe (2023). (online)- https://www.globalpolicy.org/en/publication/reforms-global-financial-architecture

United Nations. 2023. Informe de políticas de Nuestra Agenda Común 6: Reformas de la arquitectura financiera internacional. United Nations. (online)- https://indonesia.un.org/sites/default/files/2023-07/our-common-agenda-policy-brief-international-finance-architecture-en.pdf

Pedroso Cuenca, Pedro. “Statement on Behalf of the Group of 77 and China”, by H. E. Mr. Pedro L. Pedroso Cuenca, ambassador extraordinary and plenipotentiary, chair of the Group of 77, at the 110th Meeting of ministers and governors of the Group of 24 (Marrakech, Morocco 2023). (online)- https://www.g77.org/statement/getstatement.php?id=231010c

Nota:

1- For more details, see the paper by José Antonio Alonso in this volume.