European Central Bank Decision-Making – Reform, Old Commitments and New Realities

Adoption of the euro by Lithuania changes the ECB’s decision-making model

* The views expressed in this article are those of the author and do not necessarily reflect those of the institutions of affiliation.

What is the new model and how will it work?

New decision-making rules apply to the European Central Bank (ECB) from 1 January 2015, the day Lithuania adopted the euro and the euro area club enlarged to nineteen. According to the new rules Governors will take turns to vote in the ECB’s decision-making body, the Governing Council. This rotation takes place with asymmetric frequency, depending on the size of euro area economies measured by their GDP and banking sector. All euro area central bank Governors will continue to participate in Governing Council meetings and discussions.

A change in ECB decision-making is necessary and desirable as the EMU advances. And yet the new model has imperfections. How does an old commitment to introduce this change serve the euro-area’s new reality? It is like taking from the shelf a fine garment picked for your graduation the day you were born and using it for the first time today, hoping that it would still be fashionable. In some ways, this readymade, still untested federal-like model seems to serve well a post-crisis EU facing euro-scepticism, austerity, democratic deficit and adversity to supranational superpowers. In other ways this twelve year-old creation lags behind crucial events the EU has experienced in the meantime – a big-bang enlargement to 28 members and the most severe crisis since the great depression.

How will the new model work?

The new system caps the number of Governing Council votes to twenty-one. As more countries join the euro, the Governing Council becomes a crowded group (including the six members of the ECB’s Executive Board plus nineteen national central bank Governors) so more efficient decision-making is needed. While the votes of Executive Board members remain unaltered, the cap effectively bears on the Governors’ participation, requiring them to rotate monthly over fifteen votes. The new model is based on a system of rotation according to economic and financial criteria. The application of the new voting rules was once delayed in 2009, when they were initially foreseen to enter into force as the euro area enlarged to sixteen members.

The economic and financial criteria take into account (i) the share of a country in aggregate EU GDP, with a weighting of five-sixths; and (ii) the country’s share in the total aggregated balance sheet of monetary and financial institutions (MFI), with a weighting of one-sixth. Based on these weights, country groups with different voting frequencies are created.

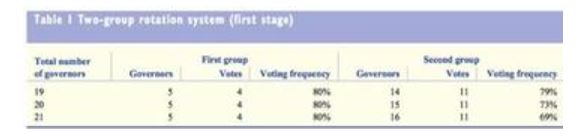

Group 1, comprising the first five largest countries, will have a voting frequency of 80% (as five countries rotate over 4 votes) irrespective of subsequent changes in euro area membership. Voting frequency for countries outside group 1 will diminish every time a new member joins the euro area. In the beginning, when the euro area has up to twenty-one members, the Governors are divided into two groups:

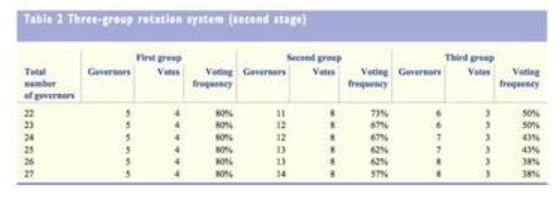

Later, when the euro will be adopted by more than twenty-one countries, voting rights will rotate across three groups:

Source: ECB, “Rotation of voting rights in the Governing Council of the ECB”, Monthly Bulletin (July 2009).

In these groups the Governors’ voting rights rotate monthly. Executive Board members hold a permanent right to vote, their votes not being subject to rotation. Currently, group 1 is composed of Germany, France, Italy, Spain and the Netherlands, while all other euro area countries are in group 2. Exact voting arrangements -the sequence according to which different Governors renounce their vote every month- were drawn up in September 2014 in the presence of all members of the Governing Council, with the Lithuanian Governor as observer. It was established that in January 2015 the Spanish central bank Governor would be the first to give up his voting right in group 1, and that the Estonian, Irish and Greek central bank Governors would be the first to do so in group 2. On 1 February 2015 the Spanish and Estonian central bank Governors regain their vote, while the French and Cypriot central bank Governors relinquish theirs in groups 1 and 2, respectively. Rotation will continue on a monthly basis according to a schedule agreed two years ahead.

Background of decision-making at the ECB

The European Central Bank came into being on 1 June 1998; it prepared the introduction of the euro as an electronic means of payment on 1 January 1999 and the entry into circulation of euro banknotes and coins on 1 January 2002; since then it has conducted the euro area’s monetary policy. During the crisis the ECB provided euro area banks with liquidity assistance and unconventional monetary policy measures. Since 2011 the ECB has hosted the Secretariat of the European Systemic Risk Board (ESRB), the first EU-wide institution with a mandate for preventing systemic risk. Since 2014 the ECB also incorporates the Single Supervisory Mechanism (SSM), responsible for supervising the euro area’s largest banks and a pillar of the banking union. The ECB Governing Council is the ultimate decision-making body for all functions currently performed by the ECB.

Until 2015, the ECB applied a voting system established in 1993 by the Maastricht Treaty. The system allowed full representation of all euro area countries irrespective of country size, putting on equal footing the votes of all national central bank Governors and those of the ECB’s Executive Board members, under the principle of one member one vote. The Maastricht Treaty (or the Treaty of the European Union) stands out as a highly reforming piece of EU legislation that put in place several founding blocks of the European Union and the economic and monetary union (EMU), among which the euro convergence (or Maastricht) criteria, the ECB and the European System of Central Banks (ESCB), the euro, the single market and the pillar structure of EU policy. The voting system established in the Maastricht Treaty served well during the first sixteen years of ECB policy-making.

As the EU became simultaneously larger and more integrated, changes were called for at various levels of governance. The treaty that tried to tackle such institutional reform was the Treaty of Nice (2003), the last one signed by an EU with a reduced number of member states (fifteen). Although ECB reform was not formally in the agenda of Nice, it belongs to the same category of measures taken at the time, such as the revision of voting rules in the EU Council. The ECB reform stems from an “enabling clause” (Art. 5) of the Nice Treaty, which stipulates that ECB decision-making procedures could be modified after the Treaty had been signed. Only two days after the Nice Treaty entered into force, the enabling clause was activated; less than two months later the reform received unanimous support from the European Council and about a year later the 15 Member States ratified the reform. This formula allowed to pass an ECB reform that: i) was not subject to political trade-offs with other institutional reforms discussed in Nice, ii) was initiated by the ECB and could not be modified by the Commission or by the European Parliament, iii) was approved by the EU’s incumbent members just before the new Member States joined the EU. Based on these considerations some authors regard the approval of the ECB rotation system as a cunning political manoeuvre.

How does the new model compare to other central banks’ voting systems?

The new ECB voting system is not unique in the world. Central banks such as the Fed and, previously, the Bundesbank employ(ed) governing formulas with selective representation of territories and a range of studies gauge the optimality of decision-making systems including such representation.

The Bundesbank’s decision-making model applied in Germany prior to the adoption of the euro. For historical reasons linked to the post war administration of Germany, the Bundesbank, founded in 1948 as the Bank of the German States, largely replicated the model of the Fed and was designed to avoid concentration of power. The governing body of the Bundesbank was composed of a six-eight member executive board designated by the federal government (Bundesregierung) and a body of nine representatives of the territories -presidents of the central banks of the Länder- designated by the federal council (Bundesrat). In the latter body, territories were represented asymmetrically: Four Länder -Baden–Würtenberg, Bayern, Hessen and Nordrhein Westfalen- had permanent representation, while the other twelve Länder shared five regional central banks and thus five representatives, with one representative from each of the groups: 1. Rheinland–Pfalz and Saarland; 2. Bremen, Niedersachsen and Sachsen–Anhalt; 3. Hamburg, Schleswig–Holstein and Mecklenburg–Vorpommern; 4. Berlin and Brandenburg; and 5. Sachsen and Thüringen. Each of the fifteen members of the governing body had one vote and decisions were taken by simple majority.

The Fed is a similar case. Its governing body, the Federal Open Market Committee (FOMC), is composed of seven members of the board of governors and five presidents of Federal Reserve Banks. Of the latter, the president of the Federal Reserve Bank of New York has permanent representation, while the other eleven Federal Reserve Banks are represented by rotation by one member for each of the groups: 1. Boston, Philadelphia, Richmond; 2. Cleveland, Chicago; 3. Atlanta, St. Louis, Dallas; and 4. Minneapolis, Kansas City, San Francisco. Rotation of voting rights takes place on an annual basis. All nineteen members participate in discussions irrespective of their current voting right. The twelve voting members of FOMC take decision by unanimity.

The ECB’s new model has a selective representation of territories like the Fed and the Bundesbank and uses rotation-based voting like the Fed, but at a higher frequency. Just like the former Bundensbank model, territories are represented in the ECB’s decision-making process based on a political criterion, since central banks Governors participate as representatives of the respective member states (i.e. political entities). This is not the case at the Fed, where the monetary policy constituencies (the districts) represented on the FOMC do not coincide with political constituencies (the states); in most cases multiple states are represented by one or two Federal Reserve Banks. In a particular case, one single state -Missouri- hosts two Federal Reserve Banks. Moreover, neither population nor GDP, but financial sector size underpins rotation in the FOMC. The most populated district (San Francisco) has the lowest voting frequency (one vote out of three); and some districts like Philadelphia have more voting power than their economic size, while others such as Atlanta and Cleveland have less.

Is there an optimal way to design a monetary policy committee?

Academic literature has devoted some attention to the optimal formula for central bank governance and the ideal design of a monetary policy committee. In a nutshell, the main finding is that the optimal design of a governing body is achievable by calibrating three dimensions -size, centralization and territorial representation in the committee. These may feature an impossible trinity because a decision making body cannot simultaneously reconcile reduced size, high centralization safeguarding central authority and full representation of territories. Calibrating the best trade-off among these three dimensions depends on the political context in which each monetary authority operates.

Thus, the optimal degree of representation of territories in a decision-making body varies across jurisdictions; this optimum emerges from a political physiology sui generis whereby each state’s monetary authority develops and perfects functions according to its own political legacy. In the case of the EMU, euro area monetary policy has been entrusted to a supranational level, which calls for a model with substantial centralization (a significant number of votes allotted to the ECB’s Executive Board); at the same time, enlargement prompts the need to limit the overall size of the decision-making body, which in turn implies a selective representation of territories in the Governing Council. As such, the conclusion is that rotation indeed represents a suitable governance system for the euro area’s monetary policy committee and the challenge is then to develop appropriate criteria for the central bank Governors’ votes.

Assessing the new model

The new model tries to simplify governance, reinforces the ECB’s Executive Board (arguably the most independent component of the Governing Council) and increases the representation of large countries with respect to small, all of which can be considered a progress. Yet this fundamentally federal model opts for a rotation mechanism based on economic and financial criteria rather than on economic and demographic. The main drawback relates to the financial sector criterion.

On one hand, adoption of economic and financial criteria reinforces country bias, a risk that treaties have striven to moderate. As Governors now perceive a higher importance attached to their nationality, this may go against the ECB statutes principle that Governors sit on the Governing Council in a personal and independent capacity as monetary policy experts acting in the interest of the euro area as a whole and not as national representatives. Some even argue that the new model risks renationalizing monetary policy, but this interpretation is not clear-cut. Supranational policy making is reinforced at the ECB by the significant role of the Executive Board; as such, even if a soft kind of “renationalization” occurred, this could be regarded as a step towards the federalisation post-crisis Europe needs. Moreover, recent studies show that scenarios in which individual members of the Governing Council would follow national objectives and bargain over interest-rate setting according to GDP weights perform better than scenarios in which all Governing Council members pursue euro area-wide objectives.

On the other hand, the size of the monetary and financial institutions balance sheets is an irrelevant and distortive criterion. To start with, the size of MFI balance sheets is not the sole aspect of interest in (monetary) policymaking; other relevant dimensions include the sector’s risk, diversity, exposure, domestic vs. foreign entities, and the size of shadow banking. Looking only at balance sheet size can generate peculiar outcomes. In Luxembourg MFI total assets amount to 1,567% of GDP; in absolute terms, Luxembourg has the 8th largest financial sector among the EU28 countries that are expected to adopt the euro. The inclusion of a financial sector size component in the composite index leads to a situation in which a very small country such as Luxembourg will in the future have the same voting frequency as a medium-large sized country such as Poland.

Why then adopt such a distortive criterion? A possible argument could be found in Fed’s model, where it is not economic, but financial size, that grants New York district a permanent position on the FOMC. However, this could not have been an argument when the new model was designed, because at that time the ECB did not have any of the bank regulation and supervision functions held by the Fed. So do the ECB’s newly acquired (prudential) functions (as host of the ESRB Secretariat and the SSM) make the financial criterion more legitimate? Arguably not. The ESRB has its separate decision-making body (including, but not limited to ECB Governing Council double hats); the SSM is well equipped with its own Supervisory Board, and prudential matters are also managed at other levels than “euro area plus” (e.g. national supervisors, EBA, etc). In this context, replicating financial considerations at multiple decision-making levels is redundant and likely to be counter-productive.

An alternative weighing system based on GDP and population would be superior. Using population would reflect the wider purpose of price stability, the benefits of which accrue to all citizens and the society as a whole, and not only to corporate and financial entities. Moreover, the capital key, a system using in equal proportions GDP and population, is already applied by the ESCB for important operations like the ECB capital subscription by EU central banks, as well as for the euro area central banks’ participation in the profit or loss derived from ECB’s seignorage. In fact, when the new model was being adopted shortly after Nice, both the European Commission and the European Parliament emphasized the need to include a population criterion. This was seen either as underpinning a new model of rotation on equal footing with GDP (Commission) or as a criterion for a double majority system whereby it would be verified that the simple majority of all Governors’ votes (former model) represented a significant share of the euro area population (Parliament). In the end, none of these ideas were taken on board and the final proposal was ratified in the form initiated by the ECB.

Last, but not least, we might ask how biting the new rotation model will be, given the Governing Council’s tradition of consensus seeking. Are considerations above much ado about nothing? An assessment of different rotation arrangements is only meaningful if the Governing Council actually puts decisions to vote. Formally speaking, the Governing Council votes and decides by simple majority. However, decisions taken by consensus were the norm before the crisis. This tradition has been somewhat broken during the crisis, as monetary policymaking has become more difficult and decisions more controversial, in particular with respect to non-standard measures.

On 1 January 2015, Lithuanian citizens started exchanging their first euro notes and coins. This change is as important as another transformation it entails – a reform of voting in the ECB’s Governing Council.

As the reform of the ECB’s voting system has been long agreed upon but its implementation delayed, there are doubts about the degree of novelty that it will bring to monetary policy. But an old commitment, like a vintage garment, can return to fashion and what matters for policy, like for vogue, is confidence.

The consequences of introducing a voting rotation mechanism in a council that traditionally made decisions by consensus are not clear-cut. The reform might not produce different outcomes from the current system if members are not asked to vote or if the Governing Council experiences groupthink or free-riding (the tendency of members to avoid dissent and take a majority’s stance when knowing that a minority position would be outvoted). Under this scenario, all Governors participating in meetings would still be able to influence every discussion and formal rights to vote may be less relevant. On the contrary, if members take a vote the introduction of the rotation model could represent the opportunity to start a new phase in ECB decision-making. The crisis stimulated more debate and differences of opinion in the Governing Council, which accords well with the new voting system and with increased transparency brought by the publication of minutes from 2015. The latter indicate there is some momentum for fresh and improved governance.